.svg)

.svg)

Thousands of global businesses can't be wrong.

Sign up for free and explore global hiring with Playroll.

Can You Pay Remote Employees in the United States Without a Local Entity?

It depends. You generally need a registered U.S. entity to run payroll directly, unless you hire workers as independent contractors or use an Employer of Record (EOR) to employ them on your behalf — and all payments must be made in USD via compliant methods such as ACH direct deposit or check.

Thousands of global businesses can't be wrong.

Sign up for free and explore global hiring with Playroll.

Step-by-Step Process for Paying Remote Employees in the United States

- Verify that the worker is correctly classified as an employee (not an independent contractor) under IRS and Department of Labor (DOL) guidelines.

- Determine the employee's primary work state and any additional states where work is performed, as each state creates separate payroll obligations.

- Register for a federal Employer Identification Number (EIN) with the IRS and open state income tax withholding and unemployment insurance (SUTA) accounts in each relevant state.

- Collect required documentation, including Form W-4, Form I-9, state withholding forms, and employee banking details.

- Set a compliant pay schedule based on state-specific pay frequency laws (e.g. weekly, biweekly, or semimonthly requirements).

- Process payroll ensuring correct federal, state, and local tax withholdings, as well as Social Security (6.2%) and Medicare (1.45%) contributions under FICA.

- Pay employees via compliant methods (ACH/direct deposit, check, or pay card) and issue itemized payslips where required by state law.

- Deposit federal payroll taxes via the IRS Electronic Federal Tax Payment System (EFTPS) on your assigned monthly or semi-weekly schedule and remit state taxes to each state's revenue or labor agency.

- File quarterly federal payroll returns (Form 941) and annual returns (Form 940 for FUTA), along with the equivalent returns required by each state.

- Issue Form W-2 to all employees by January 31 each year and file copies with the Social Security Administration (SSA) and relevant state agencies.

What Are The Legal Ways To Pay United States-Based Employees From Another Country?

Local Bank Transfer

- Best for: Employers with a registered U.S. entity paying employees via domestic ACH transfers in USD.

- Pros: Cost-effective, fast settlement via the ACH network, and widely accepted by U.S. employees and banks.

- Limitations: Requires U.S. bank accounts and state payroll registrations; cross-border funding may introduce FX costs.

- Compliance note: Payroll must comply with IRS rules and state wage payment laws; wages must be paid in U.S. dollars and reported under federal and state systems.

Direct Payroll Services

- Best for: Companies with a U.S. entity that want to outsource payroll calculations, filings, and compliance.

- Pros: Ensures accurate tax withholding, automated filings with the IRS and state agencies, and reduces administrative burden.

- Limitations: Still requires entity setup, state registrations, and oversight of multi-state compliance.

- Compliance note: Subject to IRS regulations, FICA, and FUTA; no restrictions on paying in USD, but strict reporting and deposit schedules apply. Playroll's Global Payroll services manage this end-to-end.

Employer of Record Platform Disbursement

- Best for: Foreign companies hiring U.S.-based employees without establishing a local entity.

- Pros: The EOR becomes the legal employer, handling payroll, tax filings, benefits, and compliance with IRS and state agencies.

- Limitations: Higher cost than direct payroll and less direct control over employment contracts.

- Compliance note: EOR providers manage registration, tax remittance, and reporting obligations with the IRS and state labor departments. Explore Playroll's Employer of Record services.

Contractor Payment Platforms

- Best for: Paying U.S.-based independent contractors for project-based or flexible work arrangements.

- Pros: Simplified onboarding, cross-border payments, and reduced administrative overhead.

- Limitations: Does not cover employee benefits, tax withholding, or labor law protections; higher misclassification risk.

- Compliance note: The IRS enforces strict classification rules (e.g. common law test); contractor platforms do not assume employer obligations. Explore Playroll's Contractor Management Platform.

What Taxes Do I Need To Handle for United States Employees?

- Federal Income Tax (IRS): Withheld from employee wages based on Form W-4 elections; progressive rates ranging from 10% to 37%.

- FICA Taxes (Social Security & Medicare): 15.3% total split between employer and employee — Social Security at 6.2% each (capped at $168,600 for 2024) and Medicare at 1.45% each.

- FUTA (Federal Unemployment Tax Act): Employer-paid tax of up to 6.0% on the first $7,000 of wages, often reduced to 0.6% with state credits.

- State Income Tax: Applies in most states with varying rates and rules; employers must register and withhold accordingly.

- SUTA (State Unemployment Insurance): Employer-paid contributions with rates varying by state and employer experience rating.

- Local Taxes: Apply in certain jurisdictions (e.g. New York City, San Francisco), requiring additional withholding and reporting.

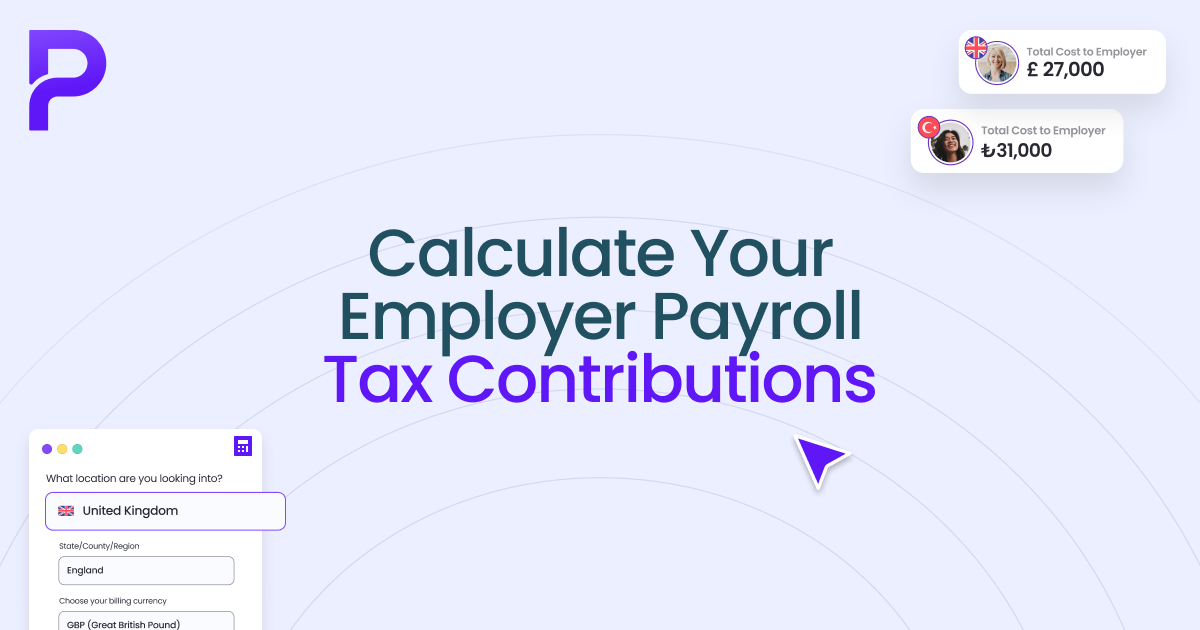

Use Playroll's payroll tax calculator to estimate your total employer costs in the United States.

What Are the Biggest Compliance Risks When Paying Employees in the United States?

- Worker misclassification (IRS, U.S. Department of Labor): Misclassifying employees as contractors can result in back taxes, penalties, and liability for unpaid benefits under federal and state laws.

- Multi-state payroll errors (State Departments of Revenue): Failing to register or withhold taxes in all applicable states can trigger audits and penalties across multiple jurisdictions.

- Payroll tax deposit failures (IRS): Late or incorrect deposits via EFTPS can incur penalties ranging from 2% to 15% of the unpaid amount.

- Permanent establishment risk (IRS): Employing workers in the U.S. may create taxable presence for foreign companies, triggering corporate tax obligations.

- Late filings and reporting penalties (IRS and state agencies): Missing deadlines for Forms 941, W-2, or state equivalents can result in fines per form, increasing with delay duration.

- Wage law violations (U.S. Department of Labor): Non-compliance with minimum wage, overtime (FLSA), or state wage laws can lead to back pay claims and penalties.

Pay Your Remote Employees in the United States

Pay your remote employees compliantly in the United States, without the heavy lifting. We support local payroll where you have your own entity or for international hires with Playroll’s EOR services.

- Accurate payroll processing: Gross-to-net processing, compliant payslips, and on-time payments — aligned with state-specific pay frequency requirements and itemized payslip obligations under state wage laws.

- Taxes & contributions covered: Registrations, filings, and remittances to the IRS, Social Security Administration, and state revenue and unemployment agencies across all relevant jurisdictions.

- Built for local compliance: We handle statutory obligations and year-end reporting, including Forms W-2, 1099, 940, and 941, as well as FUTA and SUTA filings in every state where your employees work.

Book a demo to run payroll in the United States with confidence.

Pay Globally Without Setting Up a Local Entity

01

Compliant onboarding

We confirm the right employment setup for your remote hire's country and role.

02

Accurate payroll and contributions

We pay your remote employees accurately and on time, with all local taxes and contributions handled.

03

Ongoing compliance

We handle local payroll laws, benefits, and filings as your remote team grows.

04

Dedicated support

Our team is always on hand to support you and your remote employees.

.svg)

.svg)